Analysis of Rhode Island Governor McKee's proposed Child Tax Credit

The $325 fully refundable credit would cost $36.7 million and benefit 29.2% of Rhode Island residents.

Contents

Background

Household impacts

Statewide impacts

Conclusion

On January 13th, Rhode Island Governor Dan McKee, in his State of the State address, proposed a Child Tax Credit (CTC) as part of his fiscal year 2027 budget. The fully refundable credit would replace the state's personal exemption for children under the age of 19.

We at PolicyEngine developed a Rhode Island CTC Calculator, commissioned by the Niskanen Center, to analyze the impact of potential Child Tax Credit reforms, including Governor McKee's proposal. This tool was used by the Governor's office to examine different reform options before adopting their final proposal. Read more about the tool and how it contributed to the Governor's proposal here.

Key results of the Governor's CTC proposal for 2027:

- Costs the state $36.7 million

- Benefits 29.2% of Rhode Island residents

- Reduces child poverty by 2.1%

Use PolicyEngine's Rhode Island CTC Calculator to view the full statewide results of the Governor's proposal or calculate the effect on your household.

Background#

Rhode Island currently provides a personal exemption ($5,100 in 2025) for all household members. The exemption reduces the household's taxable income, providing tax savings that rise as households move up the state's tax brackets. For example, families with income in the highest tax bracket can receive a maximum benefit of $305 per exemption ($5,100 x 5.99% = $305). Lower-income families often cannot fully benefit from the exemption, and those with taxable income below the state's standard deduction receive no benefit.

Governor McKee's proposal would replace this exemption with a $325 fully refundable child tax credit. Key features include:

- Credit amount: $325 per qualifying child

- Age eligibility: Children under 19 years old

- Refundability: Fully refundable, meaning families can receive the credit with no earnings

- Phase-out: Mirrors the personal exemption's phase-out structure. The credit amount is reduced by 20% for each $7,590 of AGI above $265,965 in 2027.

- Exemption integration: Eliminates the personal exemption for CTC-qualifying children; the exemption remains for dependents 19 and older.

Every household with a child would receive the same credit amount of $325 before the phase-out, rather than receiving tax savings determined by their income.

Household impacts#

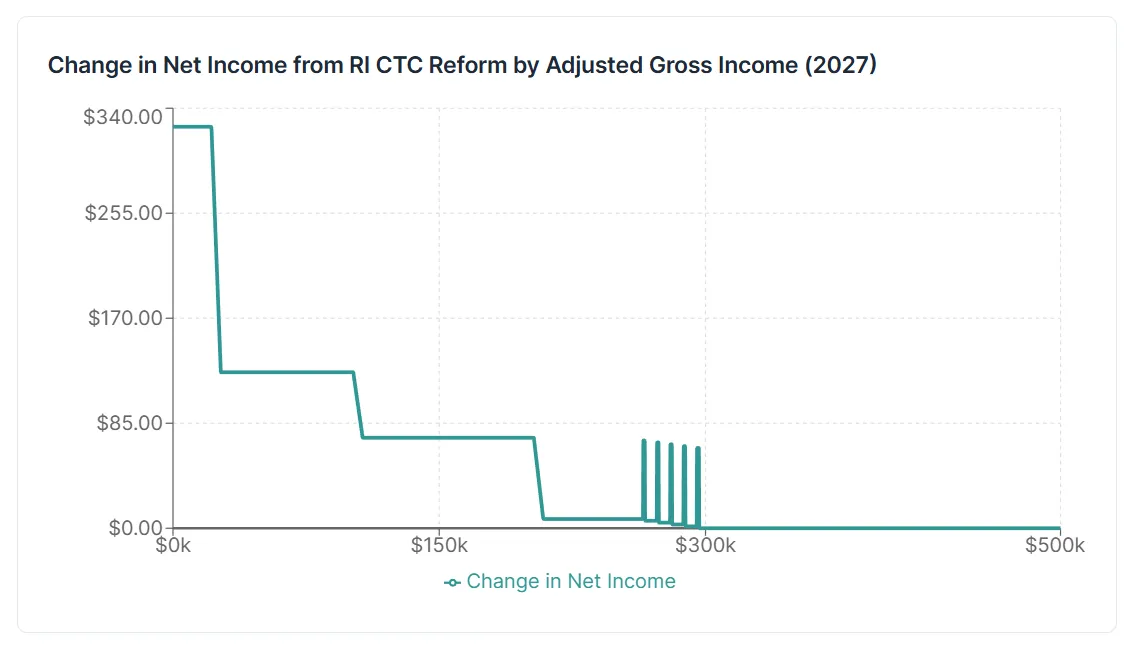

The reform primarily benefits lower-income families with children, as they see little or no benefit from the personal exemption. For example, a single parent with one child and $20,000 of AGI would see their net income increase by $325, the full credit amount. However, as AGI rises, the change in net income falls as the credit amount is partially offset by the elimination of the personal exemption for CTC-eligible children. Once the single parent reaches the top income bracket, their gain in net income is $8.1 Once the credit enters its phase-out range, their net benefit slowly drops as the CTC phase-out overlaps with the personal exemption.2 Figure 1 displays the change in net income for a single parent of one child.

Figure 1: Net income change by employment income for a single parent with one child

Figure 1: Net income change by employment income for a single parent with one child

Statewide impacts#

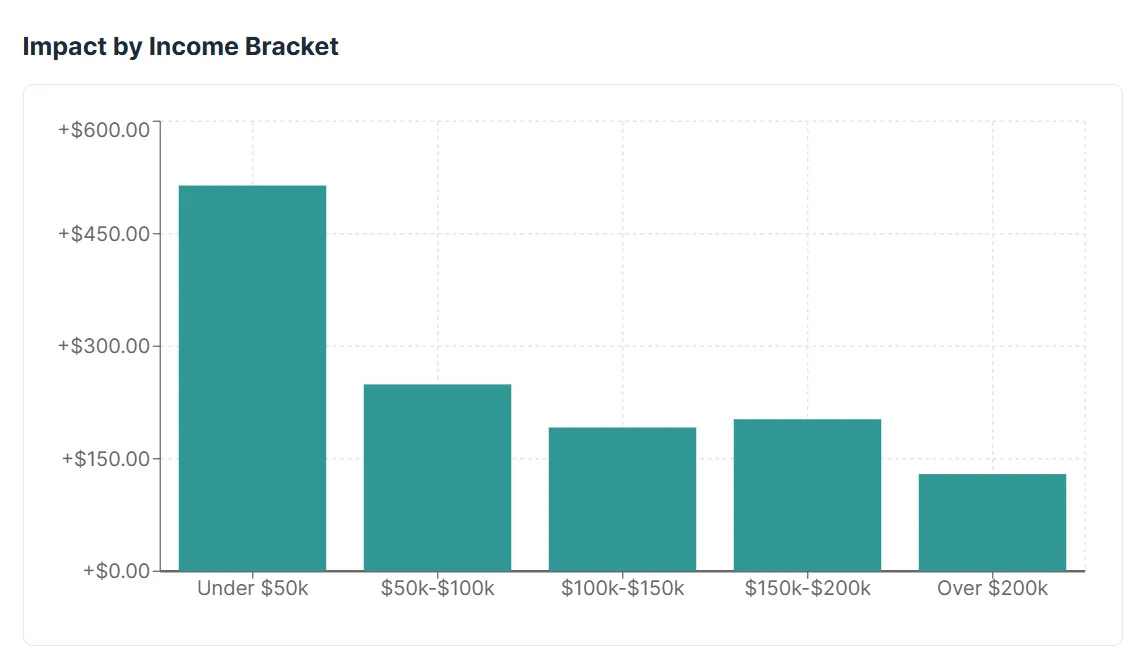

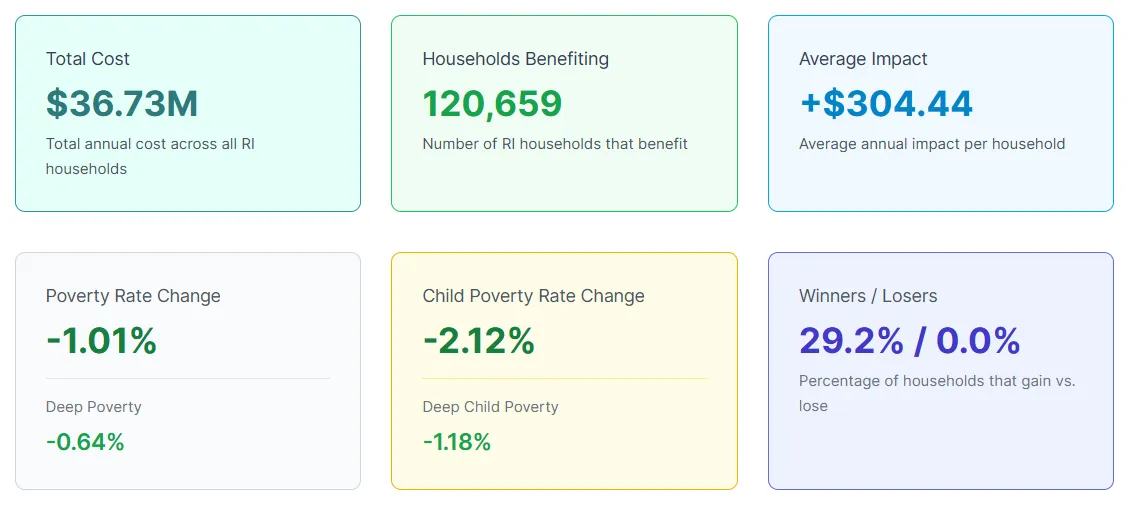

For tax year 2027, the proposal would reduce state revenues by $36.7 million, according to PolicyEngine's static modeling. The reform would also raise the net income of 29.2% of Rhode Island residents, with beneficiaries concentrated in lower income ranges (see Figure 2). We project that the proposal would reduce poverty and child poverty by 1.0 and 2.1%, respectively, as measured by the Supplemental Poverty Measure. Figure 3 displays the statewide impacts of Governor McKee's CTC proposal.

Figure 2: Average household benefit by income range

Figure 2: Average household benefit by income range

Figure 3: Statewide impacts of Governor McKee's child tax credit proposal

Figure 3: Statewide impacts of Governor McKee's child tax credit proposal

Conclusion#

Governor McKee's proposed child tax credit would replace the personal exemption with a $325 fully refundable CTC for children under the age of 19. We project the reform would benefit 29.2% of Rhode Island residents, while lowering net income for no households.

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

We invite you to explore our additional analyses and use PolicyEngine to calculate your own tax benefits or design custom policy reforms.

Explore our Rhode Island CTC Calculator to model how different Child Tax Credit designs would affect your household and the state.

-

We project that in 2027, the maximum tax savings that can be attained from the personal exemption will be $317 per person. Replacing the exemption with the $325 credit results in a gain of $8 per child for those in the top income tax bracket. ↩

-

As seen in Figure 1, the phase-out of the CTC does not perfectly align with the personal exemption, leading to instances where net income jumps suddenly. This may be due to the inflation adjustment of the CTC's phase-out parameters being rounded to a different number than the personal exemption. ↩

Research Analyst at PolicyEngine