Montana Reduces Top Income Tax Rate and Expands EITC

Montana's latest individual income tax changes will lower state revenues by $245 million and raise net income for an estimated 77% of residents in 2027.

Contents

Montana's Recent Income Tax Reforms

House Bill 337's Tax Provisions

Household Impacts

Statewide Impacts 2026

Statewide Impacts for 2027

Conclusion

On April 28, 2025, Governor Greg Gianforte (R-MT) signed House Bill 337, a bill that amends Montana's individual income tax code. HB337 reduces the state's top income tax rate from 5.9% to 5.65% in 2026 and further to 5.4% in 2027. It also raises the income threshold for the lower tax bracket for all filing statuses over two years. Additionally, the bill increases the state's Earned Income Tax Credit (EITC) from 10% to 20% of the federal EITC, beginning in 2026.

We at PolicyEngine have updated our model to reflect these changes and analyzed their effects on the state of Montana and its residents.

Key results in 2027:

-

Costs the state $245 million

-

Benefits 77% of Montana residents

-

Lowers the Supplemental Poverty Measure by 0.8% and child poverty by 3.2%

-

Raises the Gini index of income inequality by 0.16%

Use PolicyEngine to view the full results or calculate the effect on your household.

Montana's Recent Income Tax Reforms#

Montana has reformed its individual income tax policy in a series of bills beginning in 2021:

-

Senate Bill 159 (2021) lowered the state's top marginal rate from 6.9% to 6.75% beginning with tax year 2022, but left the seven-bracket structure intact.

-

Senate Bill 399 (2021) collapsed those seven brackets into two: 4.7% on the first $20,500 of Montana taxable income ($41,000 for joint filers) and 6.5% above that. It also tied the state tax base to federal taxable income instead of creating its own taxable income concept based on federal adjusted gross income, repealing some state-specific deductions.

-

Senate Bill 121(2023) lowered the top rate to 5.9%, effective tax year 2024, and increased the state's EITC match from 3% to 10%.

House Bill 337's Tax Provisions#

The reforms passed in House Bill 337 will continue to lower the tax liability for most Montana residents. As shown in Table 1, the bill lowers the state's top income tax rate to 5.65% in 2026 and 5.4% in 2027. The bill also raises the lower bracket thresholds over two years and doubles Montana's EITC from 10% to a 20% match of the federal credit.

Table 1: Montana's Individual Income Tax Parameters Before and After Passage of HB337 (2026 and 2027)

Household Impacts#

As the tax package comprises several components, different household compositions will see varying impacts to their net income. Let's examine a few examples.

For a single adult with no children and $10,000 of earnings, the tax provisions increase their net income by $69 in 2026 and $68 in 2027, solely from the doubled EITC match.

A single parent of two kids with an annual income of $50,000 will see a $252 increase to their net income due to House Bill 337: $179 from the expanded EITC, and $73 from the lower bracket threshold. In 2027, their net income rises by $266, with $205 from the EITC and $61 in reduced state income taxes. Figures 1 and 2 show the change in net income for this household as earnings rise for 2026 and 2027, respectively.

A married couple with no dependents and $200,000 of earnings will see the largest change in net income of the examined households. As their income exceeds the eligible range for the EITC, they only benefit from the reduction of Montana's top income tax rate and the expansion of the lower tax bracket thresholds. In 2026, their tax savings total $853; in 2027, their liability drops by $1,306.

Table 2: Change in Net Income Based on Household Composition

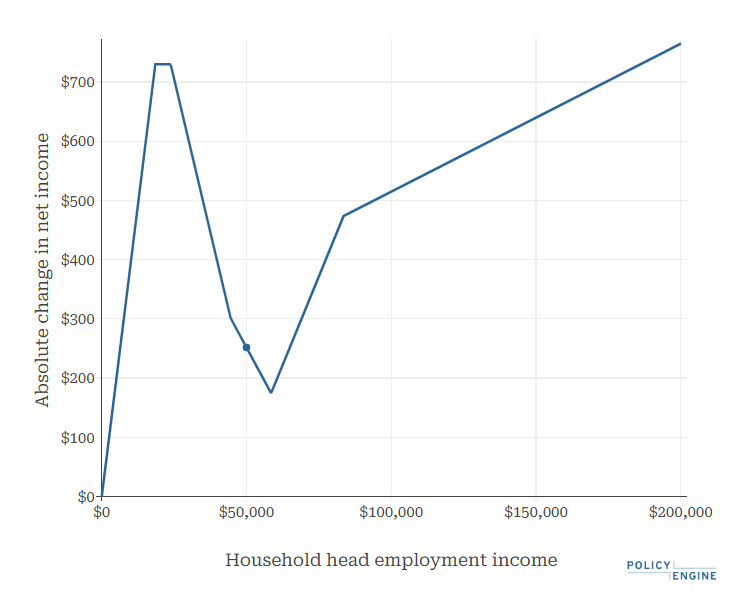

Figure 1: Change in Net Income for a Single Adult with Two Children Based on Household Earnings (2026)

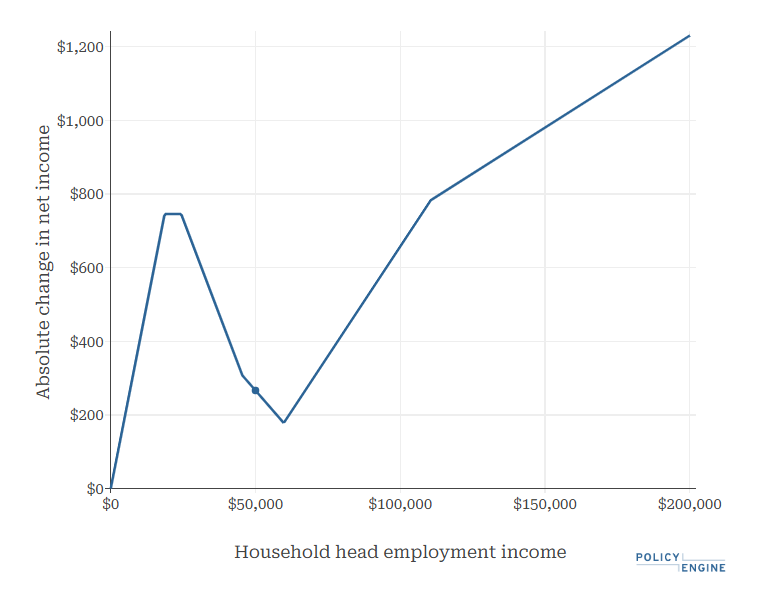

Figure 2: Change in Net Income for a Single Adult with Two Children Based on Household Earnings (2027)

A single parent with two kids initially sees an increase in their net income solely from the increased EITC. Once the credit reaches the plateau, the family's net income is raised by $730 in 2026 and $746 in 2027. Once the credit phases down, their net income falls. After the EITC is fully phased out, the household benefits only from the income tax bracket and rate changes, lowering their net income further as earnings grow.

Statewide Impacts 2026#

For tax year 2026, Montana's latest income tax changes will reduce state revenues by $167.7 million, according to PolicyEngine's static modeling based on the Current Population Survey.

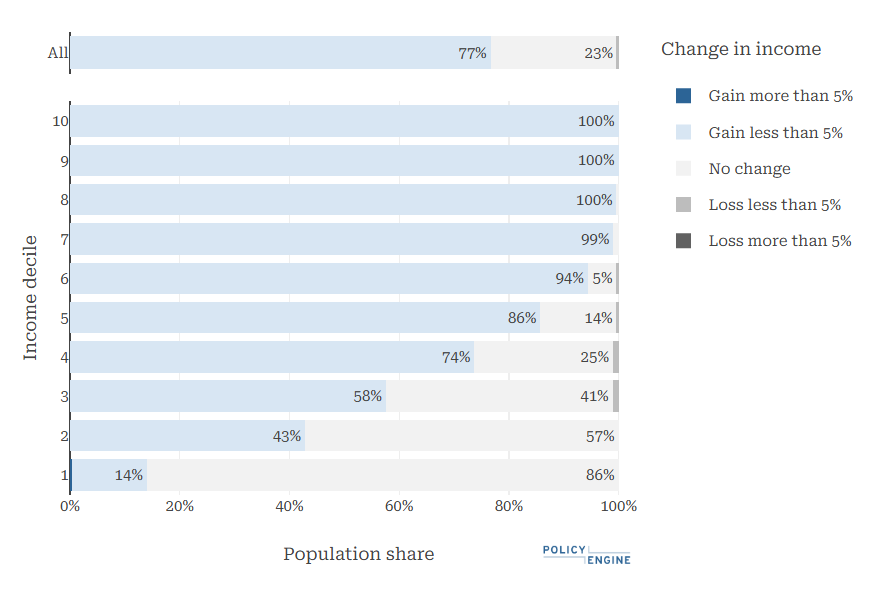

The tax changes will raise the net income of 75.9% of residents in Montana. The percentage of residents in each income decile who are net beneficiaries will vary. For example, 14% of residents in the lowest income decile will see their net income increase, while all residents in the top two deciles will see a gain.

Figure 3: Winners of Montana's Income Tax Package by Decile for 2026

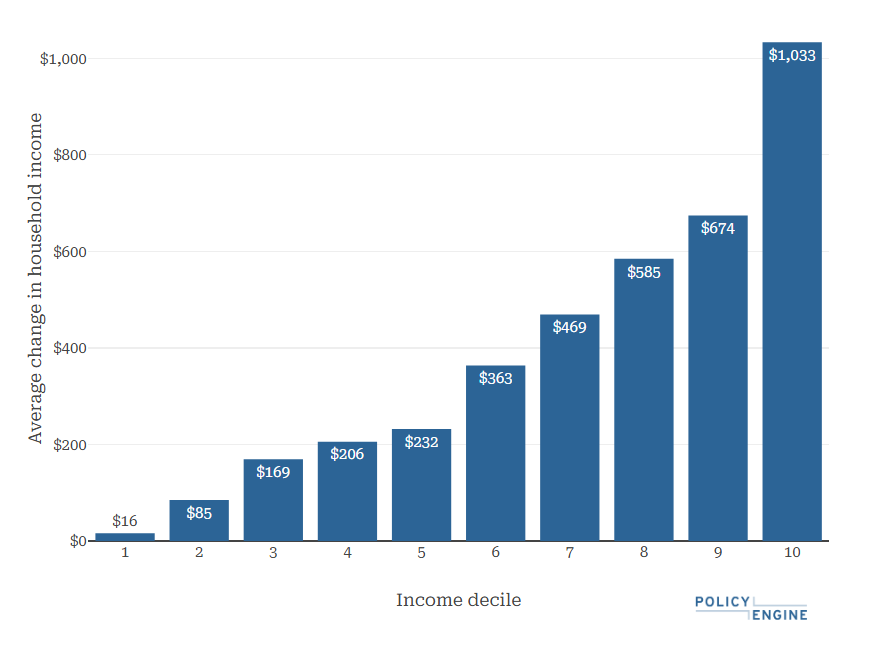

Montana's new tax package will provide an average benefit of $318 per household in 2026, ranging from $16 in the bottom income decile to $1,033 in the top decile (as defined by the nationwide income distribution).

Figure 4: Average Benefit of Montana's Income Tax Changes by Decile for 2026

We project the tax changes to reduce poverty (using the Supplemental Poverty Measure) by 0.4%, while lowering child poverty by 1.9%. The individual income tax reforms will have no impact on deep poverty.

The state's Gini index of inequality will increase by 0.05%, while the top 1%'s share of total net income will fall by 0.06%

Statewide Impacts for 2027#

In 2027, Montana's income tax changes as part of House Bill 337 will lower the state's revenues by $244.7 million, using static modeling.

Additionally, 76.7% of Montana residents will see an increase in their net income. As in 2026, the percentage of residents who are better off under the reform will vary by income decile. In the lowest decile, 14% of residents are net beneficiaries, while 100% of Montanans in the three highest deciles will see their net incomes rise.

Figure 5: Winners of Montana's Income Tax Package by Decile for 2027

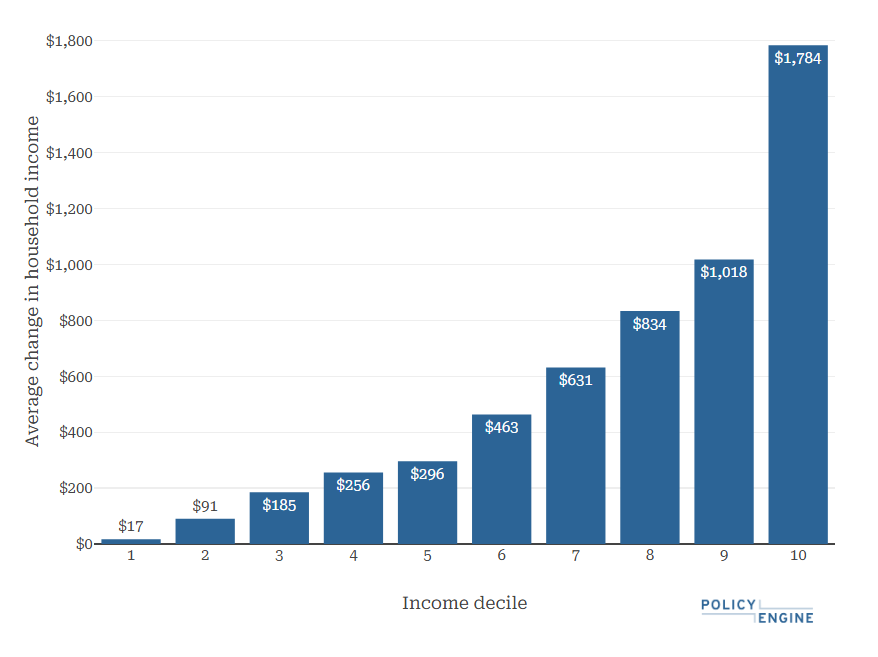

House Bill 337's provisions are projected to provide an average benefit of $456 per household in 2027. This will range from $17 in the bottom income decile to $1,784 in the tenth decile.

Figure 6: Average Benefit of Montana's Income Tax Changes by Decile for 2027

Montana's individual income tax changes will have the following effects on poverty and inequality in 2027:

-

Lower the SPM by 0.8% and child poverty by 3.2%,

-

Have no effect on deep poverty,

-

Raise the Gini index of inequality by 0.16%, and the top 1%'s share of net income by 0.05%

Conclusion#

Montana's individual tax reforms, as part of House Bill 337, will lower the state's top marginal tax rate, increase the income thresholds for the bottom bracket, and double the state's match to the federal EITC. The budgetary effect of these reforms will lower state revenues by $168 million in 2026 and $245 million in 2027. Between 76% and 77% of residents will benefit each year, with the average household benefit totaling $318 in 2026, before increasing to $456 in 2027. The net benefits will vary based on family income, but households in the top decile will receive the largest average absolute gain in 2026 and 2027. When all provisions are active in 2027, poverty in the state will fall by 0.8% while income inequality will rise by 0.16%, as measured by the Gini index.

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

We invite you to explore our additional analyses and use PolicyEngine to calculate your own tax benefits or design custom policy reforms.

Research Analyst at PolicyEngine