Manager's Amendment to H.R.1 - The One Big Beautiful Bill Act

We project that individual provisions in the manager's amendment will cost $22 billion over the budget window.

Contents

Manager's Amendment Provisions

Comparison of Discussed SALT Caps

Household Impacts

Microsimulation Results

Conclusion

Appendix A: Baseline Details

Wednesday night, the House of Representatives voted 215–214 to approve H.R.1 — One Big Beautiful Bill Act (OBBBA). The bill extends and enhances several provisions of the Tax Cuts and Jobs Act of 2017 (TCJA), while adding new individual income tax provisions such as exemptions for tip and overtime income and a deduction for auto loan interest.

Included in the passed bill by the Rules Committee is a "Manager's Amendment," which revises three tax provisions in the Budget Committee's version of the OBBBA.

These reforms include:

-

Increasing the cap on state and local tax deductions (the SALT cap)

-

Reducing the exemption and phase-out start for the alternative minimum tax (AMT) by changing its indexing year

-

Further limiting itemized deductions for high-income filers

In this report, we demonstrate the impact of the manager's amendment through hypothetical households and simulate its net effects on the U.S. against a baseline of the Budget Committee's OBBBA. We find that the changes will:

-

Decrease revenues by $22.0 billion from 2026 to 2035

-

Raise net income for 3.1% of Americans in 2026, while reducing net income for 3.3%

-

Lower the Gini index of income inequality by 0.15%

View the impact of the Manager's Amendment on the economy and your household.

Manager's Amendment Provisions#

The Ways and Means Committee introduced the initial OBBBA tax provisions on May 12th. That bill extended TCJA provisions like lower rates, a higher standard deduction, and an expanded Child Tax Credit (except for a new Social Security Number requirement), while introducing new provisions such as exemptions for tip and overtime income. It also revised three TCJA policies: the SALT cap, the AMT, and the limitation on itemized deductions.

The manager's amendment further revised these policies, while also revising other policies such as Medicaid work requirements and Inflation Reduction Act tax credits. Table 1 shows each of those policies in 2026 under current law (TCJA expiration), TCJA, the Ways and Means OBBBA, and the House-approved OBBBA (post-manager's amendment).

Table 1: Features of Individual Income Tax Provisions Revised in the Manager's Amendment (2026)

In sum, the manager's amendment:

-

Expanded the SALT deduction between the Ways and Means SALT cap and the SALT Caucus's proposed SALT cap

-

Reduced the AMT exemption amount and exemption phase-out start by changing the base year from 2017 to 2025 for inflation indexing

-

Further limits itemized deductions by effectively treating the SALT deduction as if the filer is in the 32% bracket, for those in the top (37%) bracket

Comparison of Discussed SALT Caps#

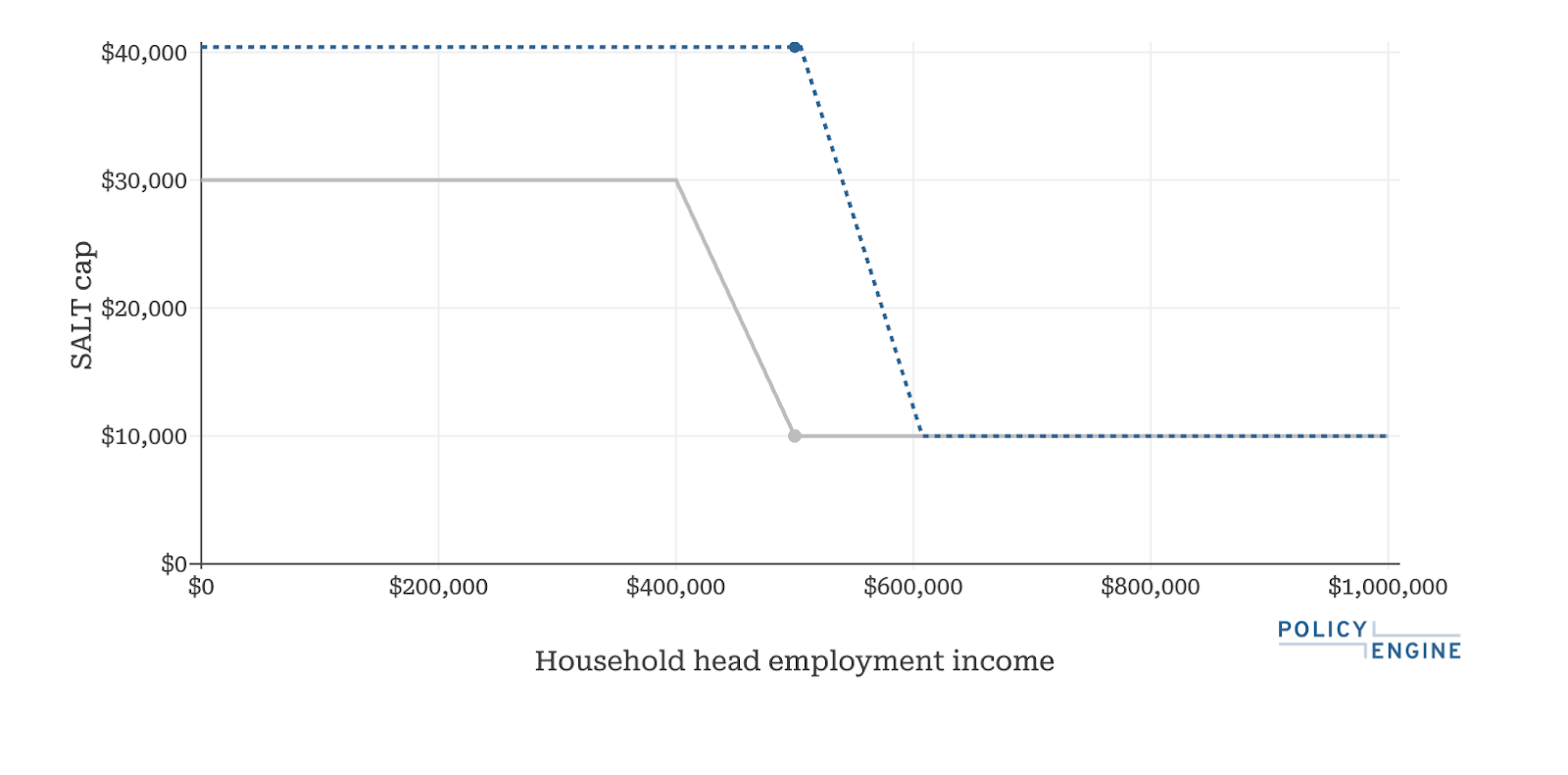

Under current law, the state and local tax deduction is set to become uncapped starting in 2026 after being limited to $10,000 under the Tax Cuts and Jobs Act. The initial draft of the OBBBA capped the SALT deduction at $30,000, and once adjusted gross income reaches $400,000, the limitation phases down at a 20% rate until reaching $10,000 (the maximum, floor, and phase-out threshold are all halved for married couples filing separately).1

Under the new compromise, households could claim up to $40,000 in SALT ($20,000 for separate filers) in 2025. Unlike the Ways and Means bill, the new SALT increase would start in 2025 rather than 2026, thus increasing the current cap of $10,000 this year. The deduction phases out at a 30% rate for filers with adjusted gross income above $500,000. The SALT cap and phase-out threshold grow by 1% each year until 2033, at which point the values would remain constant. Figure 1 displays the different SALT caps for single filers under the initial bill and the amended version.

Figure 1: Maximum SALT Deduction under the Initial W&M SALT Cap and the Manager's Amendment for a Single Filer in 2026

In addition to these changes, the manager's amendment increased the overall limitation on itemized deductions to 5/37 of the lesser of a household's total SALT deduction or the difference between their taxable income and the top income bracket's threshold. The 2/37 limitation remains for all other itemized deductions. Furthermore, the manager's amendment sets 2025 as the base year for alternative minimum tax inflation adjustments, lowering the AMT exemption amount and phase-out start. Each change will affect a household's eligible SALT deduction and effective SALT cap.

Household Impacts#

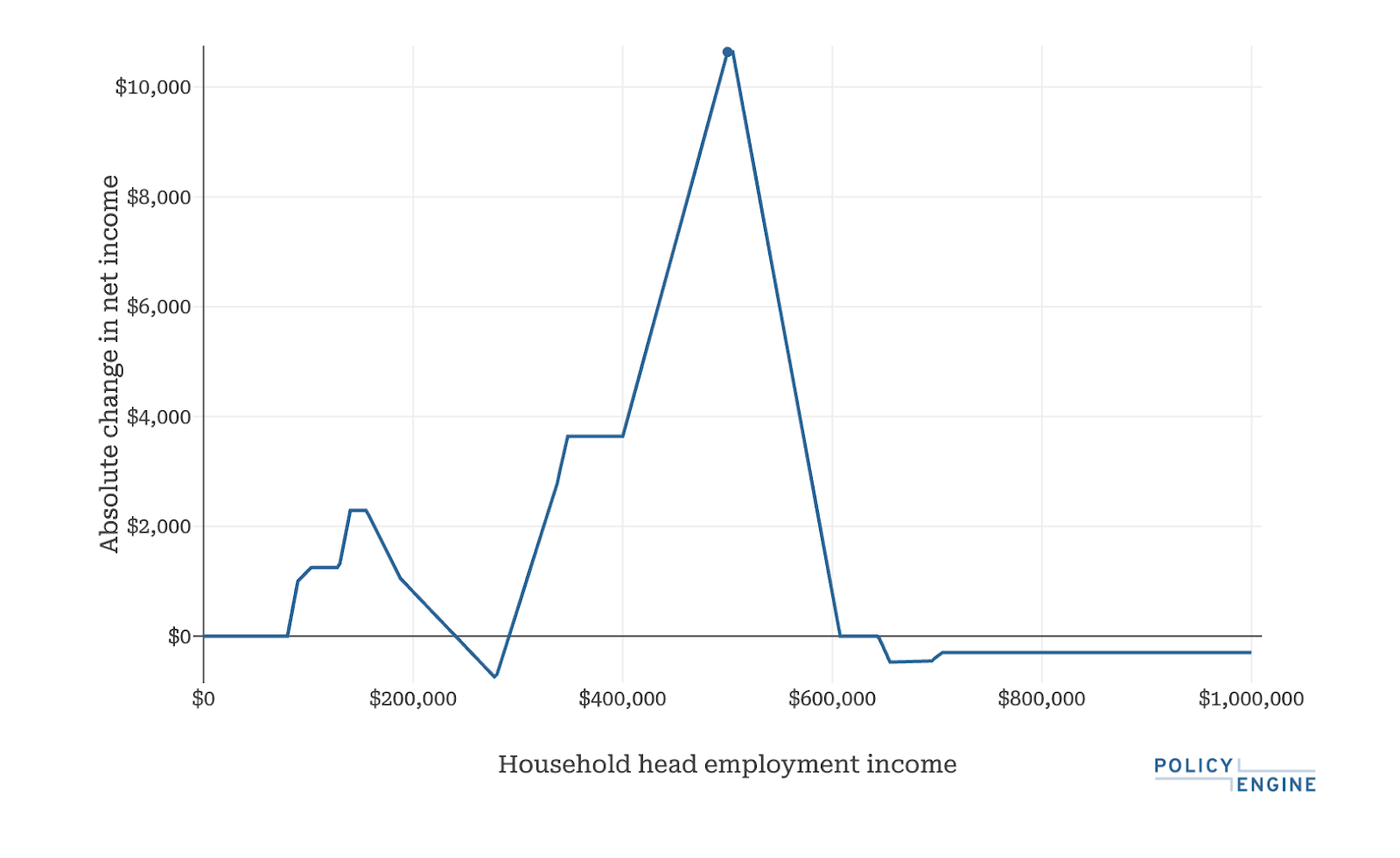

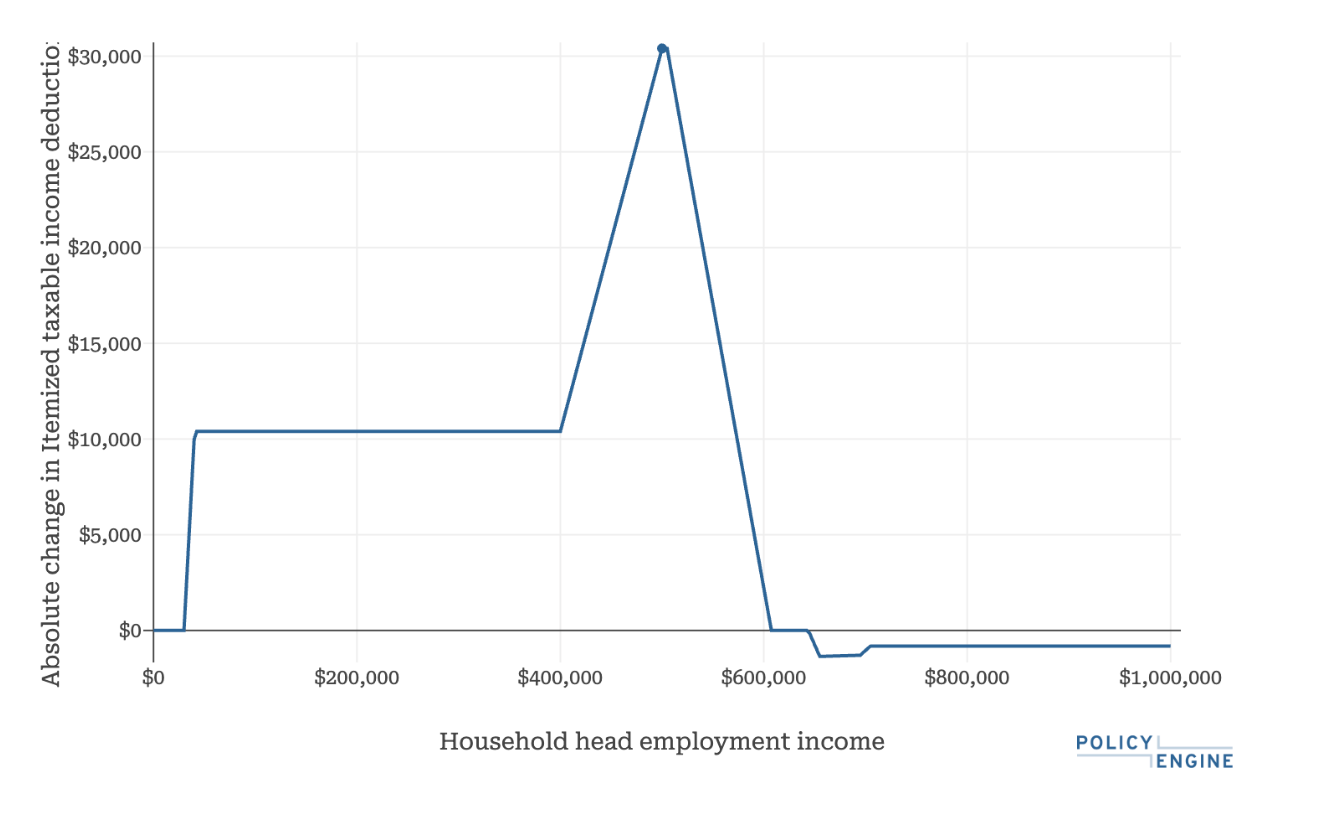

The changes to the SALT deduction, overall limitation on itemized deductions, and AMT would affect households that itemize their deductions and have state and local tax expenses greater than the initial limit in the Ways and Means bill. To understand this, let's examine a single adult in Texas making $500,000, with $40,000 in property taxes2 and $50,000 in other itemized deductions (e.g., charitable contributions or mortgage interest). Under the manager's amendment, they would see an increase in their net income of $10,640 in 2026, compared to the Ways and Means OBBBA. Figure 2 displays how this filer's net income would change as their household earnings vary.

Figure 2: Effect of OBBBA Manager's Amendment on Net Income for a Single Filer with $40k in Property Taxes and $50k in Other Deductions (2026)

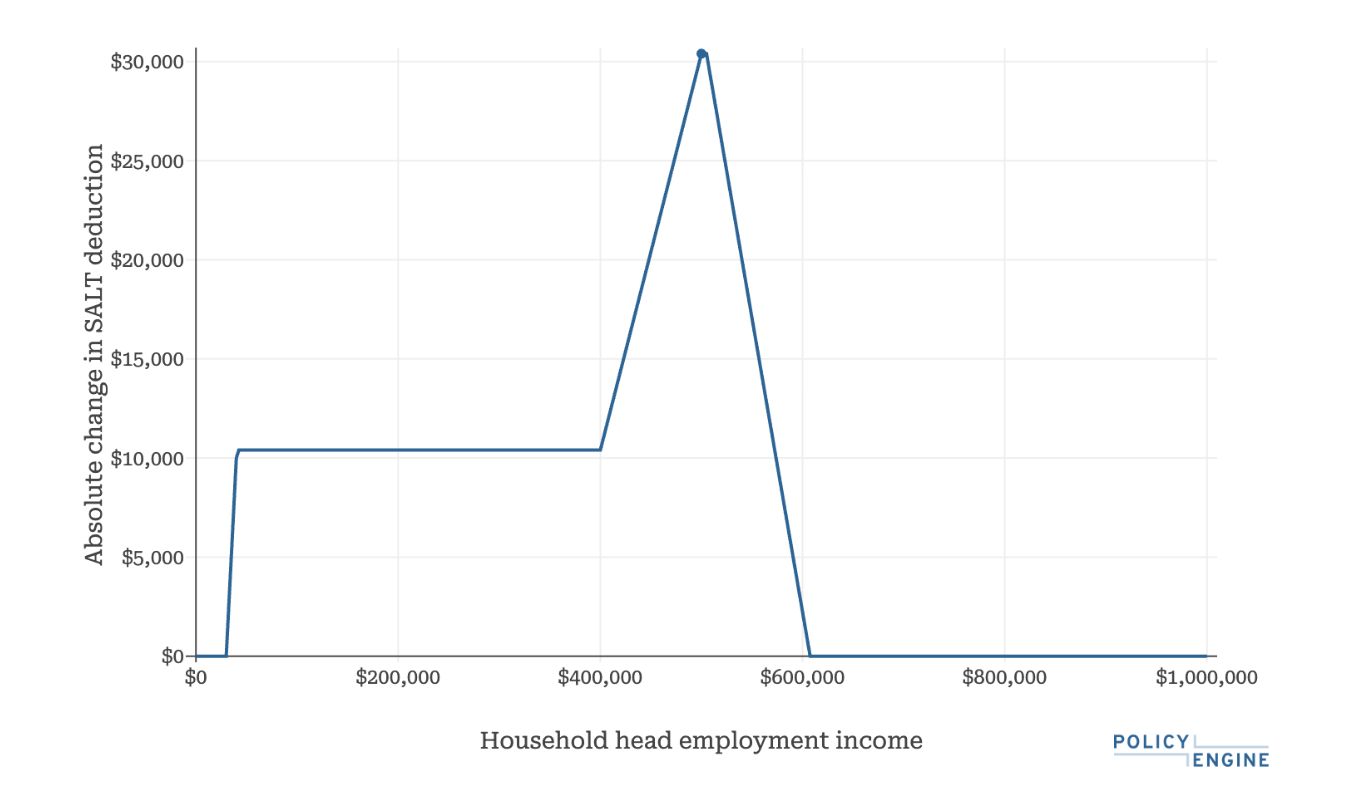

Let's dissect this segment by segment, starting at $90,000 earnings where the amendment begins to increase their net income (lower their taxes). As shown in Figure 3, this results from a $10,400 larger SALT deduction.

Figure 3: Effect of OBBBA Manager's Amendment on SALT Deduction for a Single Filer with $40k in Property Taxes and $50k in Other Deductions (2026)

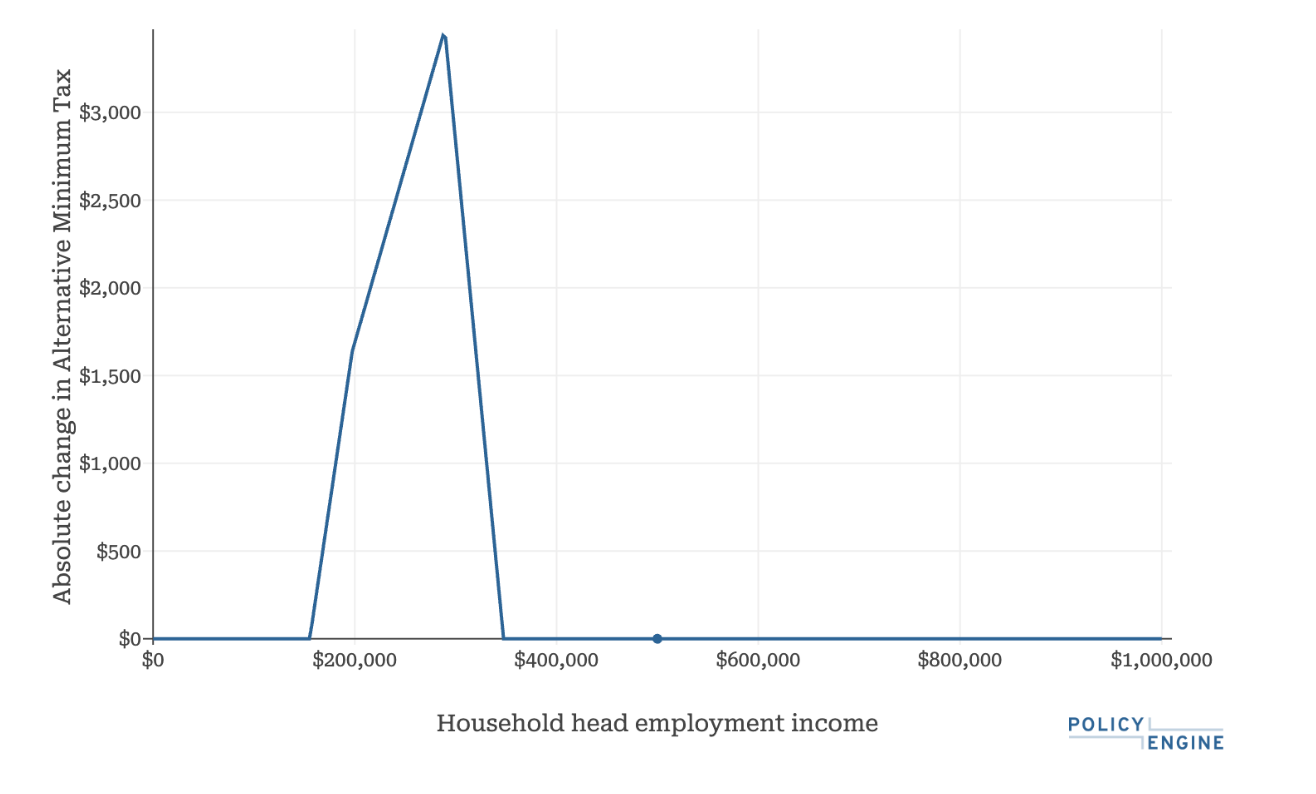

At $155,000 earnings, their net income begins to decrease, and then after the change reaches its lowest point at $277,500 earnings, it begins rising again. Figure 4 shows that these result from being subjected to AMT due to the smaller AMT exemption, and then the AMT effect phasing out.

Figure 4: Effect of OBBBA Manager's Amendment on AMT for a Single Filer with $40k in Property Taxes and $50k in other deductions (2026)

At $400,000 earnings, the filer's SALT deduction rises as the previous version began phasing out at that threshold, while the manager amendment pushed the phaseout to $505,000 in 2026. Once the household's SALT deduction begins to phase out, net income falls until reaching $0 at $606,000 of earnings. At $645,000, change in net income falls below zero due to the overall limitation on itemized deductions. Figure 5 shows these in the context of total itemized deductions.

Figure 5: Effect of OBBBA Manager's Amendment on Itemized Deductions for a Single Filer with $50k in Other Deductions (2026)

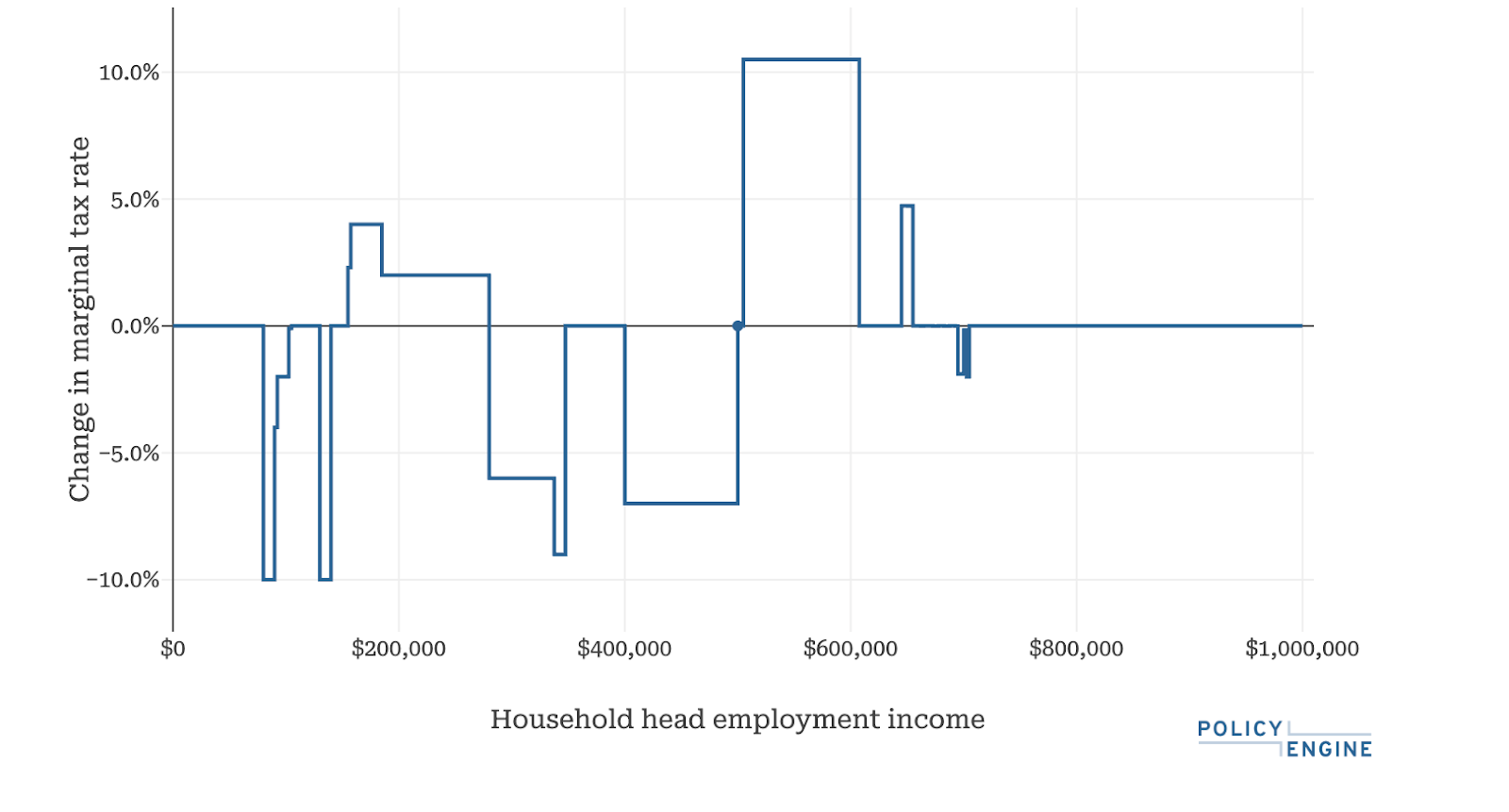

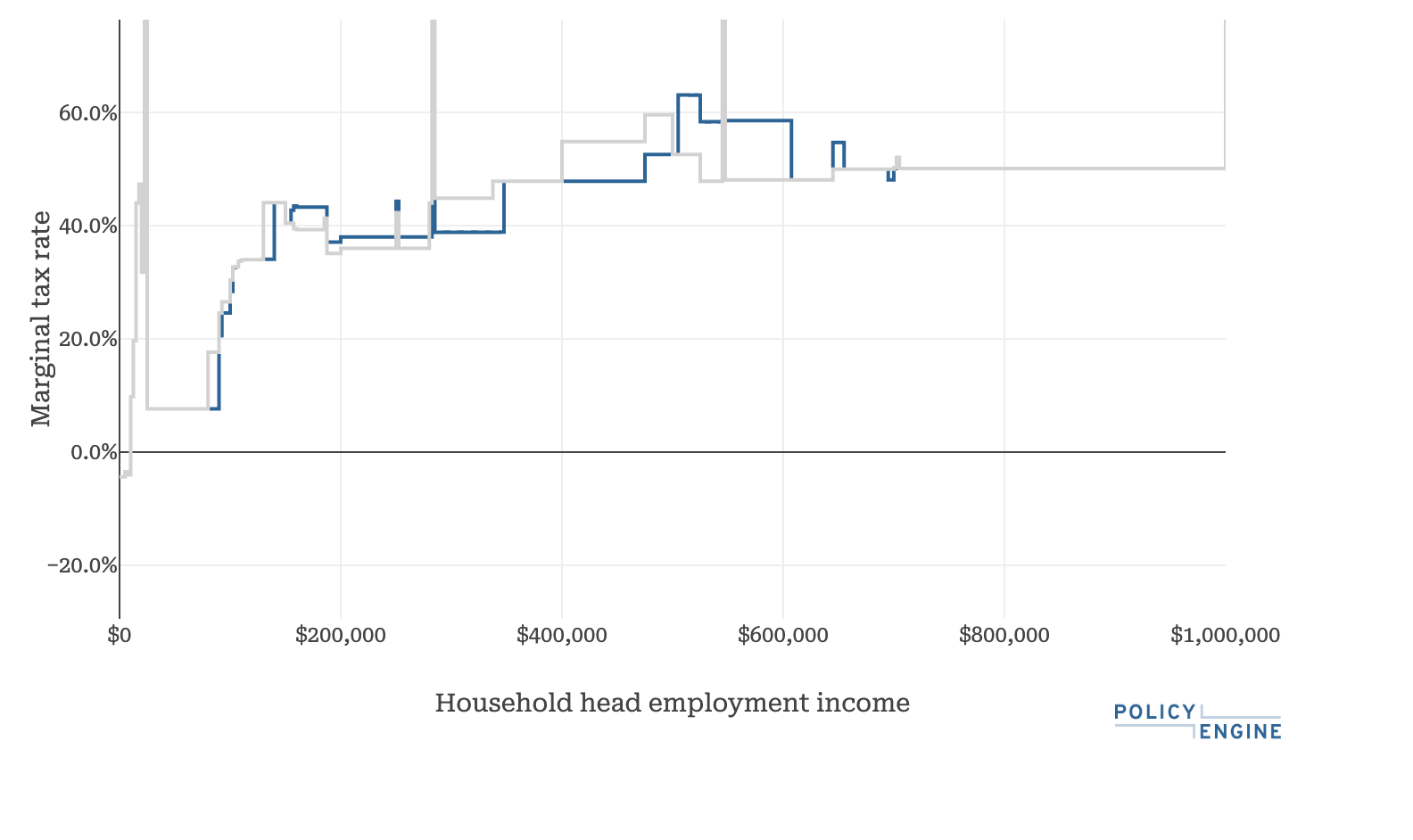

The amendment would affect the single adult's marginal tax rates (MTRs) at various earnings levels, as shown in Figure 3. Because the SALT cap no longer phases out at the $400,000 income level, the filer's MTR falls by 7 percentage points between $400,000 and $497,500. It then rises by 10.5 percentage points for earnings between $505,000 and $605,000. Finally, the SALT limitation increases MTRs by 4.7 percentage points and then lowers it at income levels where the previous would have taken effect.

Figure 6: Change in Marginal Tax Rates Based on Household Earnings for a Single Filer with $40,000+ in SALT and $50,000 in Other Deductions (2026)

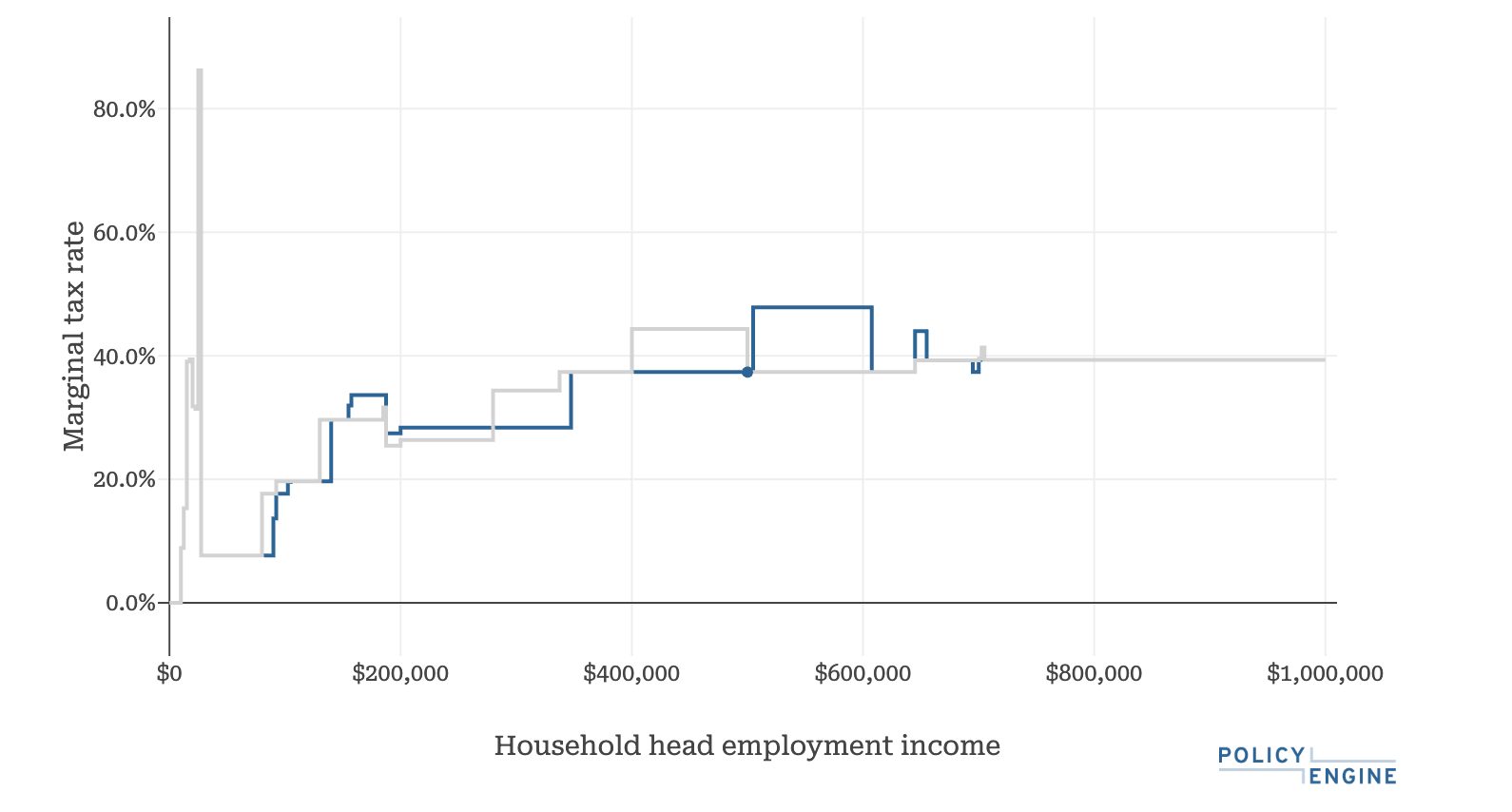

Due to the increase of the later SALT cap phase-out threshold, the total MTR increases to 47.9% for earnings between $562,000 to $605,000, its highest level above benefit phase-out income ranges.

Figure 7: Marginal Tax Rates for Single Filer Under the pre- and post-manager's Amendment OBBBA (2026)

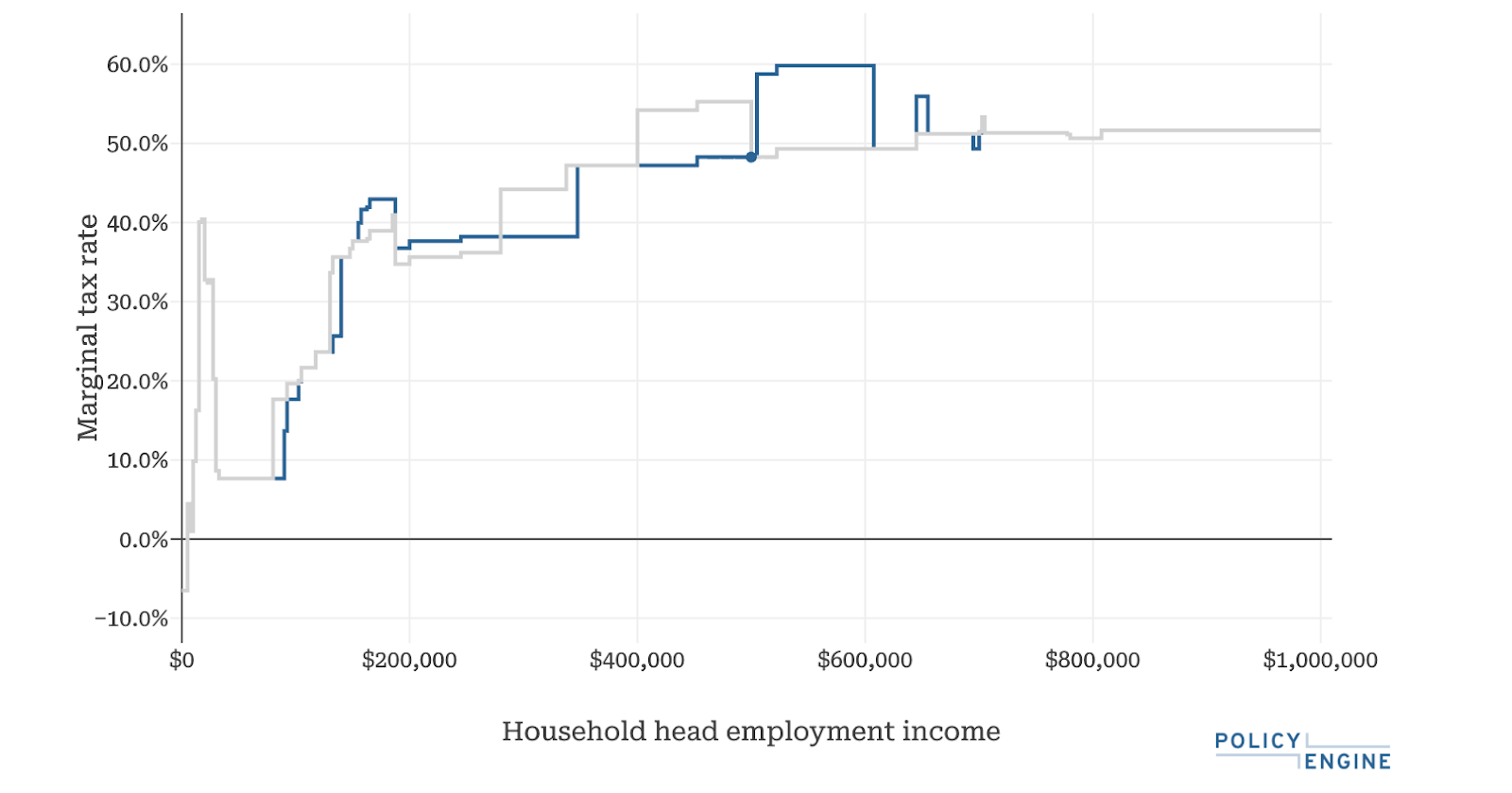

In jurisdictions with state and local income taxes, the SALT cap phase-out results in higher MTRs. For example, Figure 8 shows that this same filer would face a 59.8% MTR in California when earning between $522,500 and $605,000.

Figure 8: Marginal Tax Rates of a Single Filer in California Under the pre- and post-manager's Amendment OBBBA (2026)

The highest MTR we identified as a result of the amendment occurs in New York City, where the filer would face a 63.1% rate on earnings between $505,000 and $522,500 (see Figure 9).

Figure 9: Marginal Tax Rates of a Single Filer in New York City Under the pre- and post-manager's amendment OBBBA (2026)

Filers with different income levels and amounts of itemized deductions would experience varying changes to their net income. Table 2 shows the change in net income for several household examples in Texas.

Table 2: Change in Net Income for Various Single Adults in Texas Based on Itemized Deductions and Household Earnings

Filers in other situations, such as with high capital gains, could face larger impacts from the amendment due to the alternative minimum tax. We do not illustrate hypothetical households with these characteristics, but include them in our microsimulation analysis.

Microsimulation Results#

Using PolicyEngine's static microsimulation model, we project that the manager's amendment to the One Big Beautiful Big Act would increase the cost of the tax package by $22.0 billion over the next ten years (2026–2035).3 Additionally, because the proposed changes go into effect in 2025, it would increase federal revenues by $3.0 billion this year.

Table 3: Annual Federal Revenue Impact of Individual Provisions of the Manager's Amendment to the One Big Beautiful Bill Act

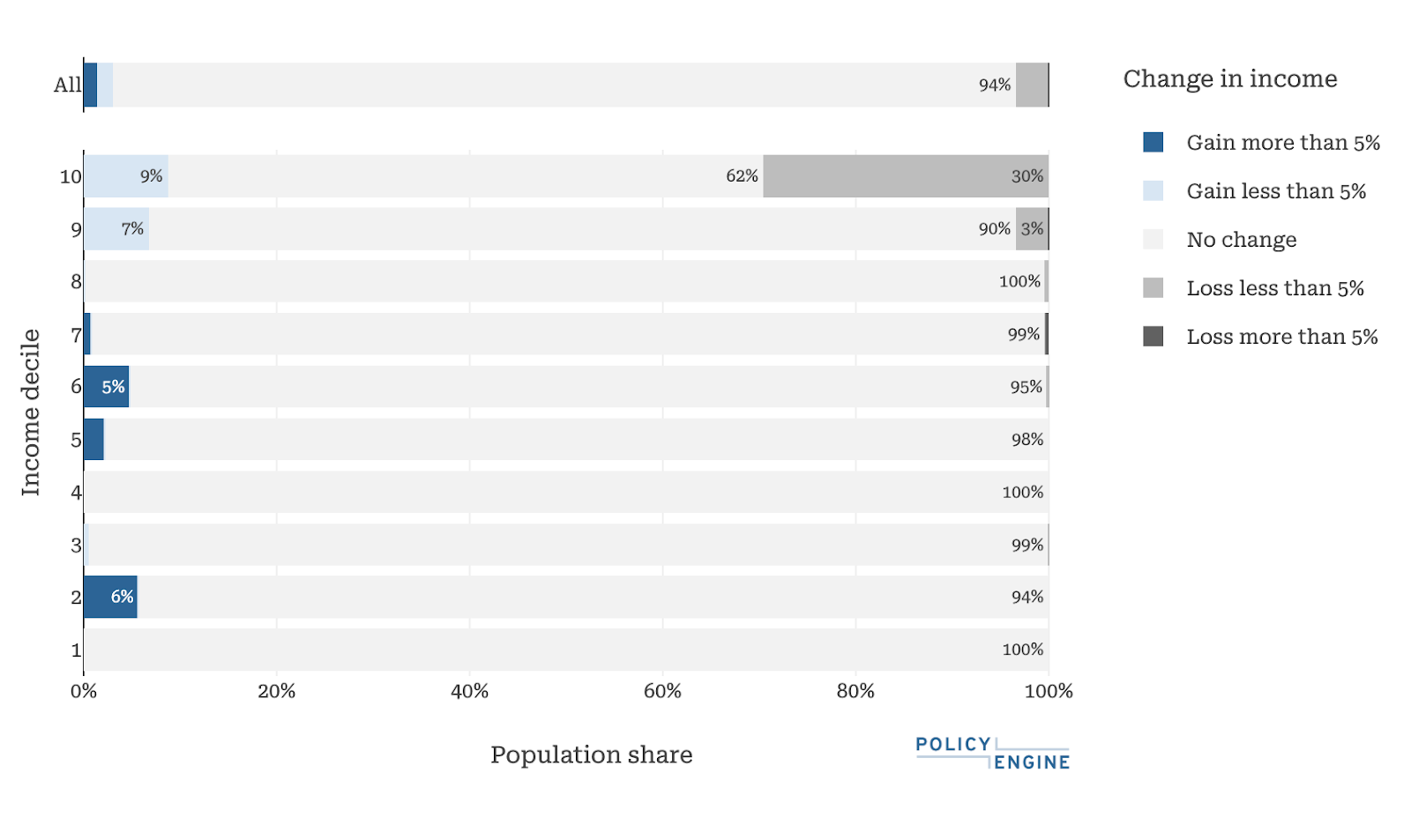

The SALT cap would increase the net income of 3.1% of US residents in 2026 and decrease it for 3.3% of the population. Of individuals in the top income decile, 30% would experience a reduction in net income and 9% would experience a gain.

Figure 10: Winners and Losers of the Manager's Amendment to the One Big Beautiful Big Act (2026)

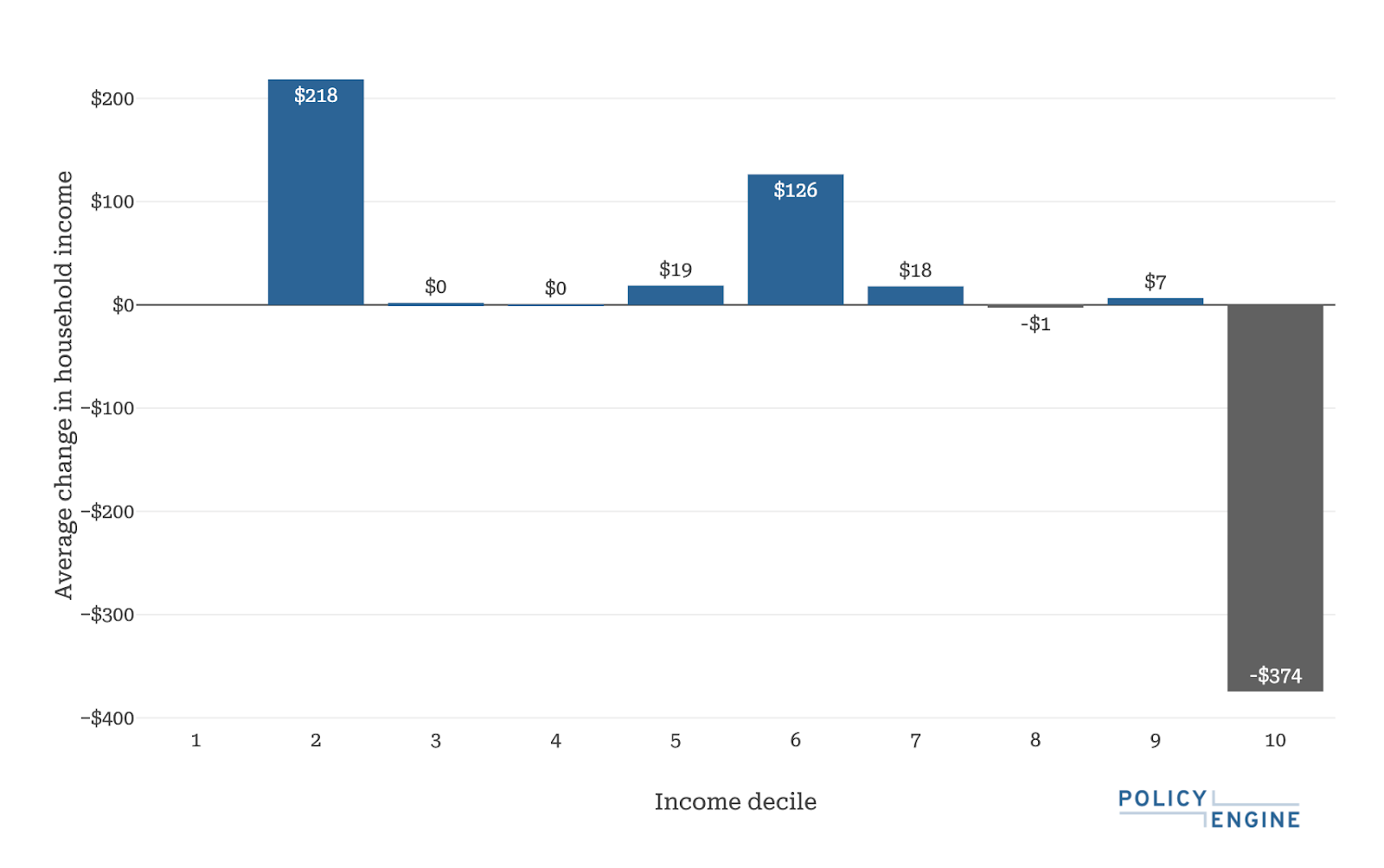

Households in the top decile see their tax liability fall by $347 on average. The second income decile would see an average gain of $218 in 2026, potentially due to some high income filers in households with low- or negative-income filers.

Figure 11: Average Impact of the Manager's Amendment to the One Big Beautiful Big Act (2026)

When it comes to inequality, the SALT Caucus proposal would, in 2026, lower the Gini index by 0.15%, and lower the top 1%'s share of net income by 0.03%

Conclusion#

The Manager's Amendment to H.R.1 — The One Big Beautiful Bill Act modifies three tax provisions originally outlined in the Budget Committee's version:

-

Expands the SALT cap from $30,000 to $40,400 in 2026

-

Reduces the alternative minimum tax exemption amounts and phase-out thresholds by changing the base year to 2025

-

Implements a higher limitation on the SALT deductions than other itemized expenses for high-income filers.

These changes would reduce federal revenues by $22.0 billion over the ten-year window when utilizing static modeling. In 2026, 3.1% of Americans would experience an increased net income and while 3.3% see their after-tax income reduce. Additionally, the Gini index of income inequality would fall by 0.15% and while the top 1%'s share of net income decreases by 0.03%.

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

We invite you to explore our additional analyses and use PolicyEngine to calculate your own tax benefits or design custom policy reforms.

Appendix A: Baseline Details#

Our baseline includes most individual provisions in the Ways and Means bill, as shown in Table 4.

Table 4: Individual Tax Provisions Current Law vs. W&M Bill

*Indexed for Inflation

-

The Ways and Means bill also includes provisions that are meant to limit workarounds that states have implemented to avoid the SALT cap. We did not model these provisions in this analysis. ↩

-

While Texas lacks a state income tax, filers can also deduct their sales tax, either reported or estimated from IRS tables. PolicyEngine calculates state sales tax from these tables, which adds between $634 and $2,677 to this filer's SALT. Combined with the $40,000 property taxes, they will exceed the $40,400 SALT cap for 2026 at all income levels. ↩

-

We project that state tax revenues would increase by $0.2bn over the budget window (2026-2035). ↩

Economist at PolicyEngine

Research Analyst at PolicyEngine

PolicyEngine's Co-founder and CEO