The 2025 American Family Act

The Child Tax Credit expansion would cost the federal government $2.5 trillion over ten years and lower child poverty by 25%.

Contents

History of Democrats’ Push to Expand the CTC

The American Family Act’s Provisions

Household Impacts

Microsimulation Results

Conclusion

On April 9th, a group of Democratic Senators and House members reintroduced the American Family Act (AFA). The bill, similar to previous versions of the AFA and Kamala Harris’s Child Tax Credit (CTC) proposal during the 2024 presidential election, would expand the credit’s size and reach for tax year 2025 and beyond.

We at PolicyEngine have updated our model to reflect the American Family Act’s proposed changes and analyzed its effect on the United States and its residents.

Key results (static):

-

Costs $2.5 trillion from 2025 to 2034

-

Benefits 42% of Americans in 2025 and 47% in 2026

-

Lowers the Supplemental Poverty Measure by 11.4% and child poverty by 25.2%

-

Reduces the Gini index of income inequality by 2.4%

Use PolicyEngine to view the full results or calculate the effect on your household.

History of Democrats’ Push to Expand the CTC#

In the past decade, Democratic lawmakers have supported several proposals to expand the Child Tax Credit. Senator Michael Bennet released his first iteration of the American Family Act in 2017, which would make the CTC fully refundable and increase the credit to $3,600 for children under 6 and $3,000 for kids 6 to 17. In 2021, President Joe Biden signed the American Rescue Plan Act (ARPA), which included the AFA for the 2021 tax year only. Senator Michael Bennet, alongside Rep. Rosa DeLauro in the House of Representatives, reintroduced the AFA in 2023, with similar parameters passed in ARPA. During her presidential campaign, Vice President Kamala Harris introduced a CTC proposal that mirrored the ARPA expansion while including a baby bonus provision that increases the credit amount for families with newborns. Neither the 2023 AFA nor Kamala Harris’ proposal was implemented, leaving the CTC at its current maximum of $2,000 under the Tax Cuts and Jobs Act of 2017. In 2026, the CTC is scheduled to revert to its pre-TCJA value of $1,000.

The American Family Act’s Provisions#

The 2025 American Family Act makes several changes to the Child Tax Credit (CTC). While the 2025 AFA shares a structure with previous versions and Harris’s CTC plan and the American Rescue Plan Act CTC, it offers larger benefits than these other CTC proposals.

Under the 2025 AFA, children under the age of six are eligible for a maximum credit of $4,320 ($360 per month), while children aged 6 to 17 would receive $3,600 ($300 per month). The 2025 AFA also contains a baby bonus where parents of newborns can claim $2,400 for the first month instead of the standard $360 monthly credit for young children. This means families with newborn children would receive a total of $6,360 during the baby’s first year. Additionally, the 2025 AFA extends the $500 nonrefundable adult dependent credit beyond its scheduled 2026 expiration date, preserving a benefit that was originally enacted in the Tax Cuts and Jobs Act of 2017.

Like the previous proposals, the 2025 AFA implements a phase-out structure with two tiers. The CTC would initially begin to decrease at $112,500 adjusted gross income ($150,000 joint). At this level, the credit’s value drops by $50 for each $1,000 of income above the threshold until reaching $2,000 for each child claimed. At $300,000 AGI ($400,000 joint), the CTC would continue to decrease at the same rate until it reaches zero. The adult dependent credit only begins its phase-out at the second threshold, where it also reduces by $50 for each $1,000 over the limit. Under the AFA, the adult dependent credit phases out simultaneously with the CTC, unlike under the TCJA, where the CTC and the adult dependent credit values are combined and then phased out. Lastly, the American Family Act eliminates the TCJA provision that requires children to have a valid Social Security Number to receive the credit; under the AFA, children with an individual taxpayer identification number (ITIN) would now be eligible.

Table 1 summarizes the key parameters of the 2025 AFA compared against the previous version of the bill and Kamala Harris’s CTC proposal.

Table 1: 2025 American Family Act, 2023 American Family Act, and Kamala Harris’s CTC Proposal Parameters

Household Impacts#

Since the 2025 AFA makes the CTC fully refundable, households with no household earnings would now be eligible for the entire credit, raising their net income. For example, a single parent with a newborn and no income currently receives no CTC. However, with the fully refundable CTC and baby bonus component, their net income would increase by $6,360, the highest gain of any household with one child.

Middle-income families with qualifying children will also see a boost to their net income. For example, a married couple with two children (ages 4 and 8) with $80,000 of annual earnings would gain $3,920. Their new CTC allotment would reach $7,920, increasing from $4,000 today.

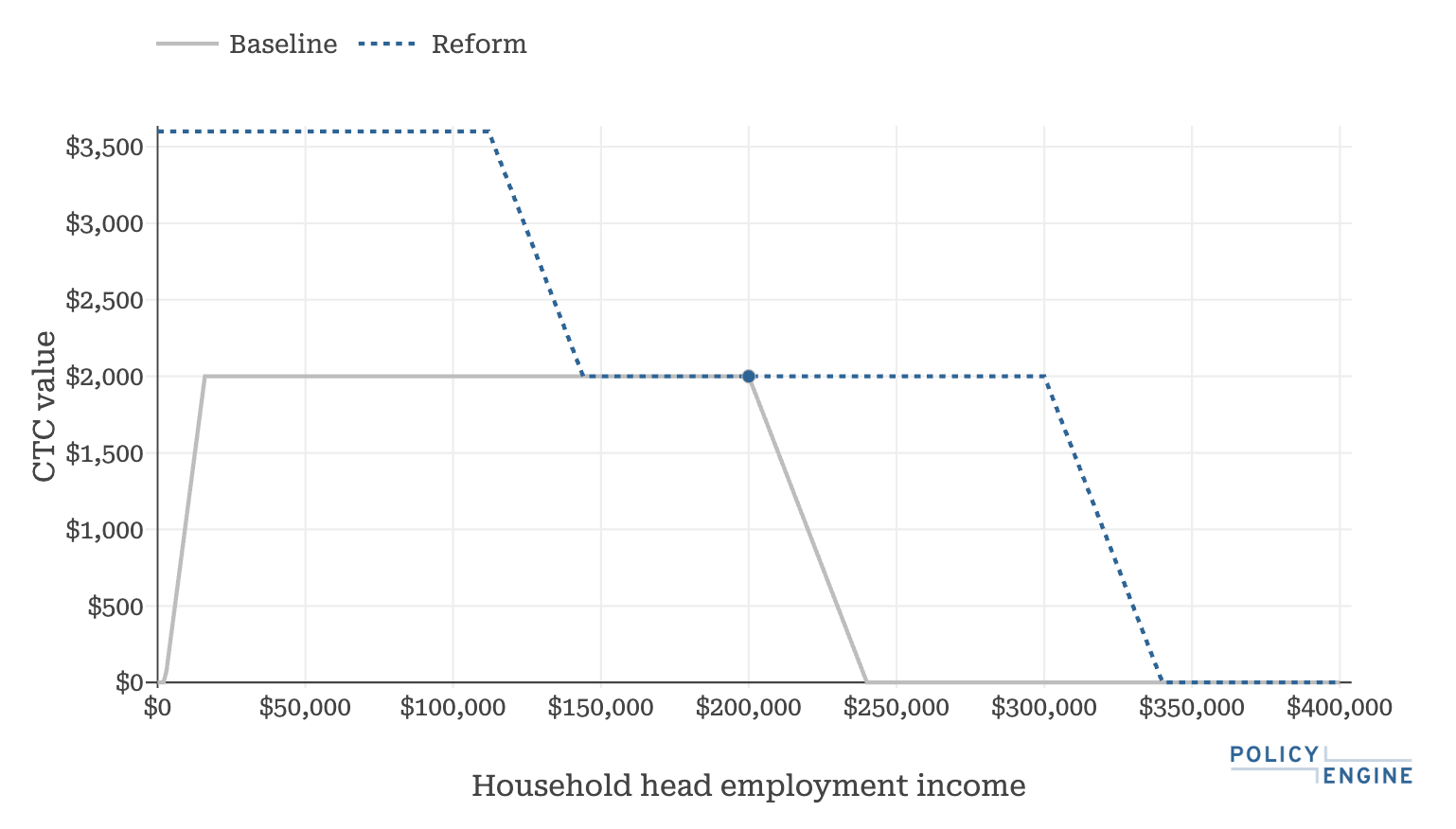

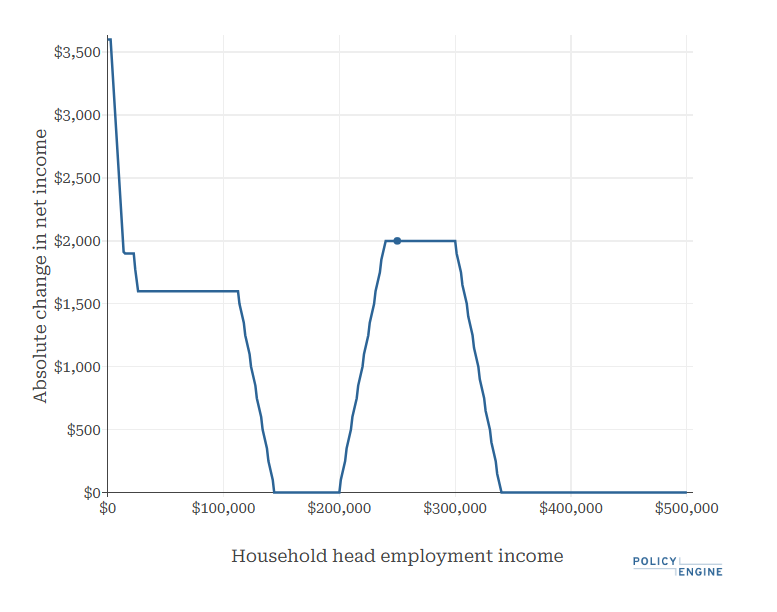

As income rises, households will be subject to the initial phase-out. A single parent with one older child and $135,000 of earnings will receive $2,450 from the CTC, resulting in a gain of $450 to their net income. As this household’s income exceeds the lower threshold of $112,500 for head of household filers, the CTC value is reduced, falling by $1,150 from its $3,600 maximum. If this family’s income fell between $150,000 and $300,000, they would receive $2,000 as the initial threshold cannot reduce the benefit lower than $2,000 per child.

However, because the current CTC begins to fully phase out at $200,000 for head of household filers, this household with $250,000 of annual earnings would see a $2,000 increase to their net income as the AFA raises the higher phaseout threshold to $300,000. Once household income reaches $340,000, the CTC fully phases out, and their change in net income falls back to $0.

The AFA leaves some married filers with both adult and child dependents worse off: consider a couple with earnings of $425,000, an adult dependent, and an 8-year-old child. As the AFA phases out — the adult dependent credit and CTC simultaneously — joint filers see a decrease in net income until the entirety of the CTC and adult dependent credit value phases out, as under current law. For this household, net income begins to fall at $400,000 before plateauing at a $500 decrease. Once the current CTC is phased out at $440,000, net income begins to rise as the remaining $500 adult dependent credit begins to phase out. At $450,000, net income stabilizes at $0. The AFA’s increased head of household phase-out threshold prevents unmarried filers from paying higher tax.

Figure 1 displays the value of the CTC under the AFA compared to current law, while Figure 2 shows the change in net income for a single parent with one older child as annual earnings vary.

Figure 1: CTC Value of 2025 AFA for a Single Parent with One Child Age 6–17 Compared to Current Law Based on Household Earnings

Figure 2: Change in Net Income of 2025 AFA for a Single Parent with One Child Age 6–17 Based on Household Earnings

Table 2 summarizes the change in net income for each household discussed above.

Table 2: Change in Net Income by Household Composition

Microsimulation Results#

Using PolicyEngine’s static microsimulation model, we project that the American Family Act will cost the federal government $167.2 billion in 2025. Over a ten-year period (2025–2034), the legislation will reduce federal tax revenues by $2.5 trillion.

Table 3: Annual Federal Budgetary Impact of the AFA

Because the TCJA’s CTC provisions expire for tax year 2026, the cost of the AFA increases as the CTC’s value is projected to fall to $1,000 compared to its current maximum of $2,000. In addition to the federal budgetary impact, the AFA will reduce state revenues by $35 billion over ten years due to interactions with the CTC provisions.

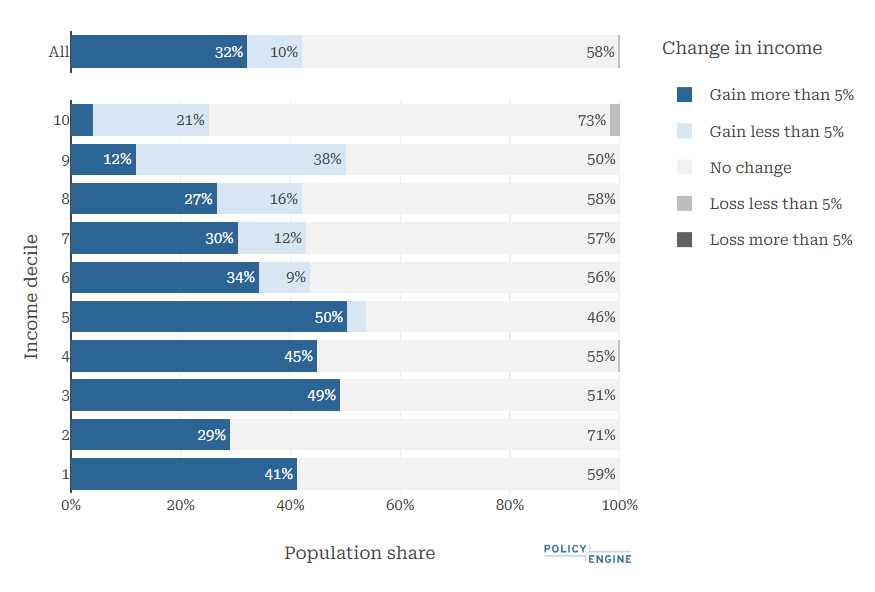

The AFA will raise the net income of 42.1% of American residents in 2025, including 25% of those in the top income decile and 54% of those in the fifth decile. Additionally, 1.7% of people in the top income decile would see their net incomes decline due to the adult dependent phasing out independently of the CTC rather than as one combined value. In 2026, when the TCJA expires, the AFA will increase the net income of 46.7% of people, while leaving no households worse off, since the adult dependent credit expires with the TCJA.

Figure 2: Winners of the AFA (2025)

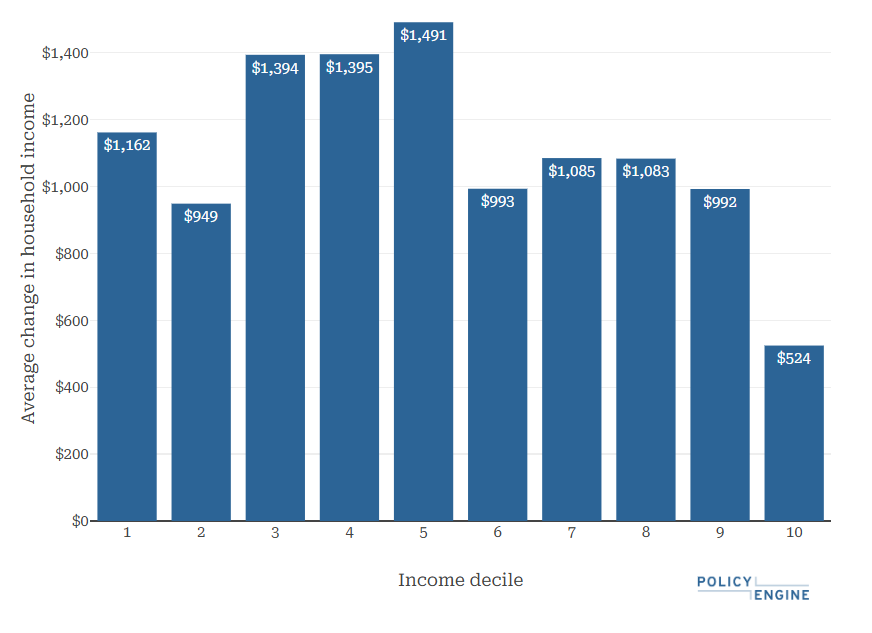

The AFA is projected to provide an average benefit of $1,115 per household. Families in the fifth decile would see the highest average benefit at $1,491, while the top decile would see the lowest gain of $524, due to the credit phaseouts. When examining average benefit by percent of net income, the first decile receives the largest gain, then decreases by each subsequent decile. In 2026, the average household benefit increases to $1,540.

Figure 3: Average Benefit of the AFA by Decile (2025 and 2026)

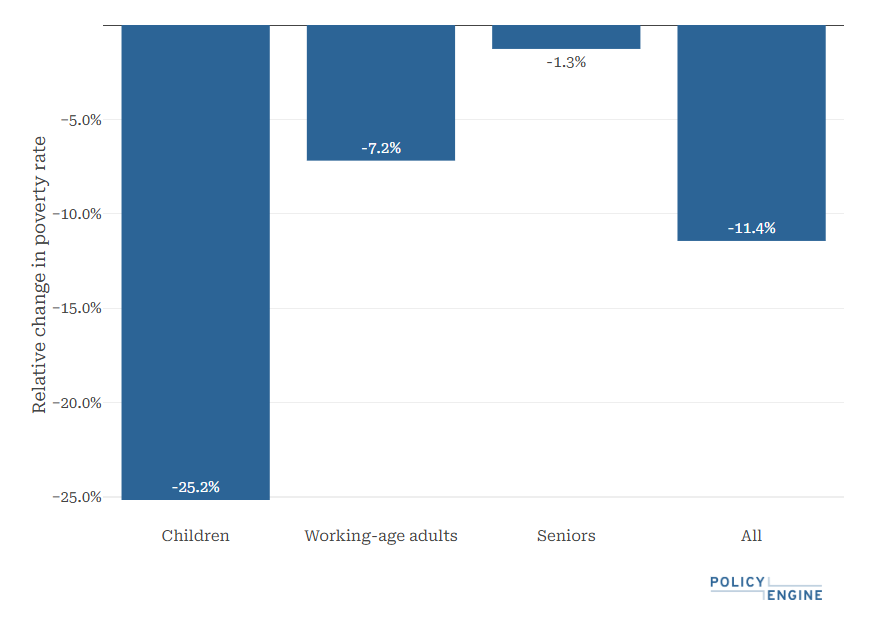

The child tax credit expansion would reduce poverty (as defined by the Supplemental Poverty Measure) by 11.4% and child poverty by 25.2% in 2025. Deep poverty and deep child poverty would fall by 12.2% and 29.9%, respectively. These poverty statistics vary by less than six percentage points across years in the 10-year budget window.

Figure 4: Poverty Reduction Under the AFA (2025)

Finally, the AFA will reduce the United States’ Gini index of inequality by 2.4%. The bill would also reduce the top 10% and 1%’s share of net income by 0.4% and 1.0%, respectively. In 2026, the Gini index is projected to fall by 2.8%.

Conclusion#

The American Family Act will expand the Child Tax Credit by making the credit fully refundable and increasing its size for each eligible child. Over the next ten years, the AFA will reduce federal revenues by $2.5 trillion, assuming no behavioral responses. The proposed legislation will benefit 42% of the population in 2025 and provide an average benefit of $1,115 per household, varying by income decile. The AFA is projected to reduce child poverty by 25% and deep child poverty by 30% in 2025. Beginning in 2026, TCJA’s expiration results in a higher counterfactual cost and impact (poverty, inequality, and population share affected) than in 2025.

As policymakers evaluate reforms such as these, analytical tools like PolicyEngine offer critical insights into the impacts on diverse household compositions and the broader economy.

We invite you to explore our additional analyses and use PolicyEngine to calculate your own tax benefits or design custom policy reforms.

Research Analyst at PolicyEngine